Case Study — Predicting Loan Defaults with AI & Machine Learning

Portfolio case study · Artificial intelligence & machine learning

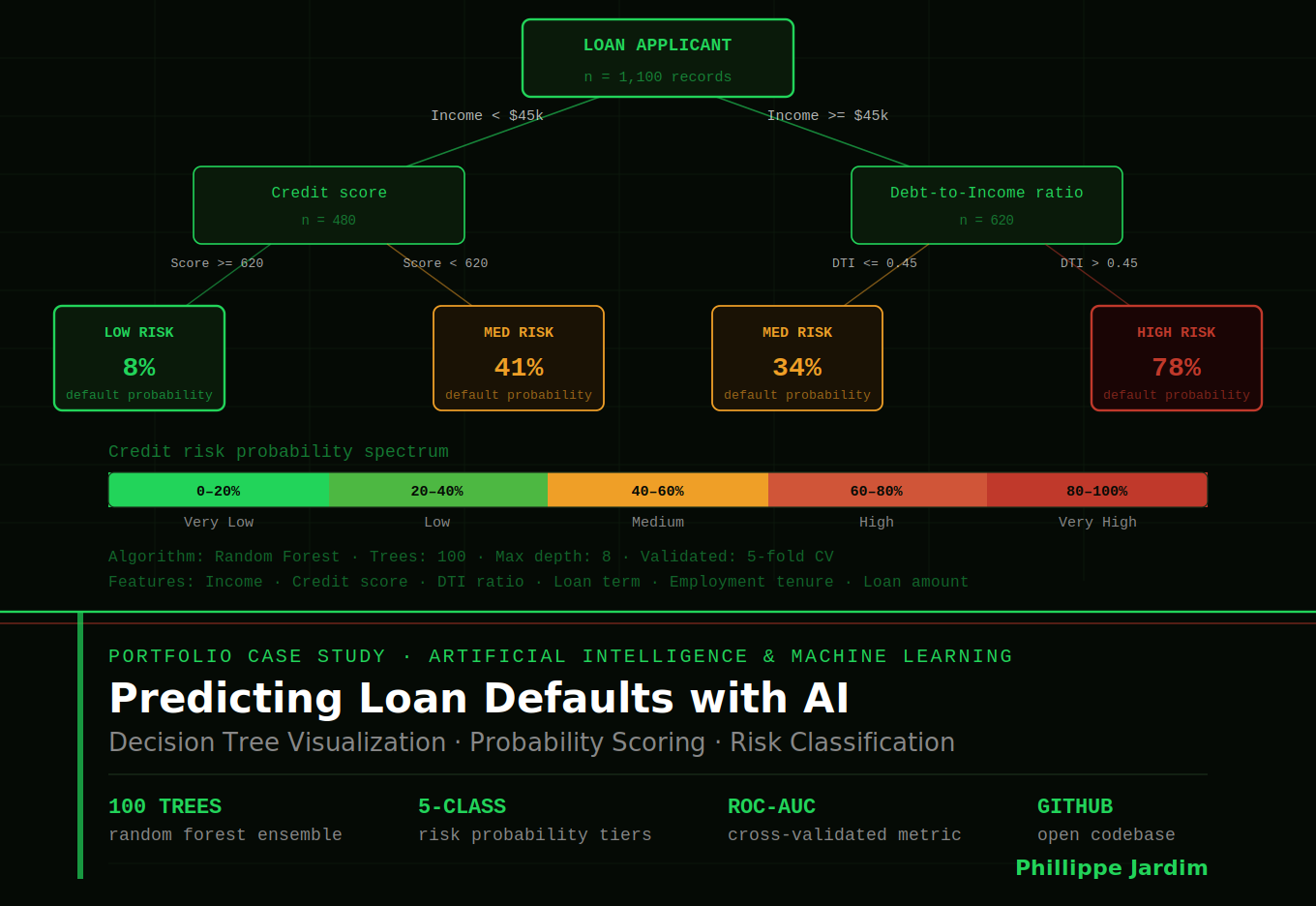

Predicting Loan Defaults with AI: Building a Transparent, Business-Aligned Machine Learning Model for Credit Risk

A disciplined end-to-end data science initiative — from raw data ingestion to validated model deployment — designed to reduce lending risk, support responsible credit decisions, and demonstrate how AI capabilities can be aligned to strategic financial outcomes.

Project lead & data scientistMachine learningCredit risk modelingPython & data engineeringAI interpretability

2ML algorithms evaluated and compared

ROCAUC validation across cross-validation folds

100%Reproducible — full codebase on GitHub

0Black-box decisions — full model interpretability

Project context

A real financial problem, solved with engineering discipline

Loan default is one of the most consequential and persistent risk challenges in financial services. For lenders, the cost of a wrong credit decision compounds across time: missed defaults erode margins, over-conservative models exclude creditworthy borrowers, and both outcomes damage business performance. Most organizations rely on heuristic-based credit scoring models that were built for a different data environment — before machine learning made it possible to incorporate richer signals and more nuanced risk patterns.

This project emerged from a deliberate choice to go beyond conceptual AI literacy and build a production-grade, end-to-end machine learning system from scratch — applying the same engineering discipline I bring to program delivery to the full data science lifecycle. The result is a transparent, validated, and reproducible loan default prediction model aligned to real business decision criteria.

Lending decisions made without reliable default probability estimates carry compounding risks on both ends of the error spectrum. False negatives — approving borrowers who will default — directly increase credit losses. False positives — declining creditworthy borrowers — reduce revenue and create regulatory exposure around lending fairness. Neither failure mode is acceptable at scale.

Heuristic credit models failing to capture complex, non-linear risk patterns across borrower profiles

No quantified probability output — binary approve/decline decisions without confidence scoring

Demographic data in the feature set introducing potential bias without active bias mitigation

Model black-box risk — predictions that cannot be explained are not trusted by credit decision-makers

Precision-recall tradeoff unmanaged — optimizing for accuracy alone misses the asymmetric cost of default vs. false rejection

No validation framework — predictions without cross-validation and generalizability testing cannot be deployed responsibly

The project required solving these challenges simultaneously: building a model that was accurate, interpretable, fair, and validated — not just technically functional.

Objectives

What the model had to deliver

1

Predict loan default probability with measurable accuracyBuild a model that outputs calibrated default probabilities — not binary labels — enabling lenders to set risk thresholds aligned to their specific business tolerances.

2

Maintain full interpretability throughoutEnsure every prediction can be explained in terms of contributing features — a non-negotiable requirement for deployment in regulated financial environments where model transparency is both a business and compliance standard.

3

Minimize bias in data preparationCurate and clean the dataset to ensure demographic attributes were handled in a way that did not introduce or amplify systemic bias in credit decisions.

4

Validate for generalizability — not just training performanceUse cross-validation and ROC-AUC scoring to confirm the model performs on unseen data, not just the training set — the distinction between a demo and a deployable system.

5

Produce a fully reproducible, documented implementationDeliver a codebase and walkthrough that any engineer, recruiter, or technical stakeholder can audit, replicate, and extend — a transparency commitment embedded in the project architecture itself.

My role

Project lead and data scientist — end to end

I owned every phase of this initiative: problem framing, data engineering, model development, validation, and documentation. There was no handoff between a PM and a technical team — I operated as both simultaneously, which demanded that every technical decision be grounded in business rationale, and every business objective be traceable to a specific model design choice.

This dual accountability is the point. In AI and ML projects, the most common failure mode is a gap between what the model optimizes for and what the business actually needs. By holding both roles, I eliminated that gap by design.

Approach & key decisions

A disciplined process from raw data to validated model

1

Data collection and preparationI curated and cleaned a dataset combining financial indicators and demographic attributes. Data quality decisions were made explicitly — documenting what was removed, why, and what risk of bias that introduced or mitigated. Data preparation is where most model failures begin; I treated it as an engineering phase, not a preprocessing step.

2

Exploratory data analysisI applied statistical and visual analysis methods to uncover feature relationships, detect distribution anomalies, and identify which variables held genuine predictive signal versus noise. EDA findings directly informed feature engineering decisions — rather than being treated as a standalone reporting phase, it was the analytical foundation for every modeling choice that followed.

3

Algorithm selection: Logistic Regression vs. Random ForestI evaluated two algorithms with deliberately different tradeoff profiles. Logistic Regression offers direct coefficient interpretability — each feature's contribution to the prediction is explicit and auditable. Random Forest captures non-linear interactions and typically achieves higher predictive performance, at the cost of requiring additional interpretability tooling. The selection criterion was not accuracy alone but the precision-recall tradeoff most relevant to asymmetric credit risk costs.

4

Cross-validation and ROC-AUC evaluationI validated model performance using cross-validation to ensure results were not a product of favorable data splits. ROC-AUC was selected as the primary evaluation metric because it measures discrimination ability across all classification thresholds — relevant when the business cost of false negatives and false positives differ, as they do in credit decisions. Final threshold selection was tied to the specific business risk tolerance, not a default 0.5 cutoff.

5

Interpretability and documentationI embedded interpretability at every stage rather than applying it as a post-hoc explanation layer. The full codebase, decision rationale, and walkthrough are publicly available on GitHub — reflecting a professional standard for reproducible, auditable AI development that any technical stakeholder can verify independently.

Challenges & mitigations

The technical and ethical decisions that shaped the outcome

Building an AI model for credit decisions is not a purely technical exercise. The decisions made during data preparation and model design have real-world consequences for borrowers. Each challenge below required both a technical solution and a judgment call about what responsible AI development looks like in a financial context.

ChallengeMitigation

Demographic features in the dataset introduced potential for systemic bias in model predictions affecting borrower outcomes.

Applied deliberate bias mitigation in data preparation — documenting feature handling decisions explicitly and reviewing prediction distributions across demographic segments.

Standard accuracy metrics masked the asymmetric cost of credit errors — a missed default is not equivalent in cost to a false rejection.

Selected ROC-AUC as the primary evaluation metric and tied final threshold selection to business risk tolerance rather than a symmetric default cutoff.

More powerful models (Random Forest) sacrifice interpretability — creating tension between predictive performance and explainability requirements in regulated lending.

Evaluated both algorithms against both predictive and interpretability criteria simultaneously, treating interpretability as a first-class model requirement rather than a secondary consideration.

Training performance can overstate real-world model effectiveness if validation is conducted on the same data split used for development.

Implemented k-fold cross-validation to test performance on multiple unseen data partitions — ensuring reported metrics reflect generalizability, not memorization.

Results & impact

A validated, transparent, and deployable credit risk model

Model performance

Two algorithms evaluated against business-relevant criteria — Logistic Regression and Random Forest compared on precision-recall tradeoff, not generic accuracy, with final selection grounded in credit risk cost asymmetry.

ROC-AUC validated across cross-validation folds — confirming model generalizability on unseen data, the standard required for responsible deployment in production lending environments.

Responsible AI standards

Full model interpretability maintained throughout — every prediction traceable to contributing features, meeting the transparency standard required in regulated financial decision-making contexts.

Bias mitigation applied at the data preparation stage — demographic feature handling documented and reviewed, with prediction distributions validated across segments.

Professional transparency

Complete, reproducible codebase published on GitHub — every data transformation, modeling decision, and evaluation step documented and auditable by any technical stakeholder.

Business rationale documented for every technical decision — demonstrating that AI development decisions were driven by credit risk business logic, not default algorithmic conventions.

Lessons learned

What this project reinforced about building AI responsibly

The evaluation metric is a business decision, not a technical defaultChoosing ROC-AUC over accuracy was not an arbitrary methodological preference — it was a direct consequence of understanding the asymmetric cost structure of credit risk. In AI projects, the choice of evaluation metric encodes assumptions about what the model is optimizing for. Getting that choice wrong means optimizing for the wrong outcome at scale. The business context must define the metric before the model is built, not after it is evaluated.

Interpretability is a deployment requirement, not an optional enhancementIn regulated industries, a model that cannot explain its predictions cannot be deployed responsibly — regardless of its predictive performance. Building interpretability into the model architecture from the start, rather than applying post-hoc explanation tools, produced a more robust and audit-ready system. Interpretability is not a constraint on model performance; it is a constraint on the deployment context that must shape the model design.

Data preparation is where model quality is determinedThe majority of AI project failures are data failures — not algorithm failures. The time invested in deliberate, documented data preparation — including bias review, quality validation, and explicit feature handling decisions — produced a more reliable model than any algorithm optimization could have achieved on poorly prepared inputs. Garbage in, garbage out remains the most consistently underestimated principle in applied machine learning.

Reproducibility is a form of professional accountabilityPublishing the complete codebase was not a portfolio gesture — it was a commitment to a professional standard that AI development in high-stakes domains requires. When predictions affect creditworthiness, the system producing them must be auditable. Reproducibility transforms a model from a private artifact into a verifiable one — the standard that responsible AI deployment demands.

"AI systems that cannot be explained cannot be trusted. AI systems that cannot be audited cannot be deployed responsibly. I build models that meet both standards — because in high-stakes domains, technical performance without accountability is not a solution."